There are a handful of car finance options available, each with their own benefits and drawbacks. Here we’ll look at the main ones and list the pros and cons. We’ll also explain the factors you need to consider to get the best car finance.

Hire Purchase

This is an old-school way of financing a car. A finance company owns your motor. You pay a deposit and monthly repayments for the privilege of driving it. Your monthly repayments are calculated taking the price plus agreed interest, minus any deposit. This is then split into monthly payments over an agreed term, usually four or five years. At the end of the period, you will own the car.

Pros: Regular, manageable car finance payments rather than a lump sum. The loan is secured on the vehicle.

Cons: You don’t own the car until you’ve repaid the debt. You’re paying for the vehicle depreciation, as you do when buying with a lump sum. It’s complicated to end early.

Personal Contract Purchase (PCP)

This is a popular way to fund a car purchase because it’s so flexible. You and the finance company agree an annual mileage and how much the car will be worth at the end of the three or four-year term – its Guaranteed Future Value (GFV).

You then pay a deposit, which along with the GFV (also called a balloon payment) is subtracted from the car’s sticker price. The remaining sum is divided into monthly payments. At the end of the agreed period, you can either hand the car back and walk away, put any difference between its GFV and trade-in value as a deposit towards another vehicle, or pay off the GFV and own the car.

Pros: Flexible at the end of the term. It can prove cheaper than other finance methods. You can tailor your monthly payments to your needs. Sometimes car manufacturers pay the deposit for you.

This is becoming an increasingly popular way for people to buy a car because it can be cheaper than a PCP. It is the private version of leasing a car; you are essentially renting the car. At the end of the agreed period, you hand it back and start again. You pay an agreed deposit followed by monthly repayments over the term. But as with a PCP, you’re essentially just paying for the vehicle’s depreciation, hence why it’s cheap.

Pros: Lease companies frequently include servicing contracts in the monthly fee. There are low monthly rental costs. It’s very straightforward.

Cons: You can never own the car. There can be harsh penalties for early termination, exceeding agreed mileages and wear and tear conditions.

Traditional loan

This is probably the most straightforward. You decide the amount you want to borrow, then arrange it with a loan provider. Assuming you put the money you’ve borrowed towards a car, the loan isn’t secured on that car. That means you won’t lose the car if you can no longer keep up the repayments.

Pros: You own the car outright. It’s very flexible: should you need to terminate the agreement early you simply sell the car .

Cons: Just as when you own a car, you’re paying for the car’s depreciation. The sum is usually limited to £25,000.

What do I need to look at?

As with any finance, you must pay attention to the detail of car finance deals before you sign on the dotted line. Otherwise, you could be tied into something that is either very expensive to get out of, ruinous for your credit score and possibly even a drain on your sanity.

It’s important to remember that not all car finance deals are created equal. And not all car finance deals are suited to all buyers. Here are the things to look for when signing up to car finance deals. There have also been instances of mis-selling car finance products. Read more about it here.

What is the monthly payment?

The headline figure, the thing that draws you into paying for your new car on finance will be the amount you pay monthly. There are some very attractive deals around. You could run a new car for as little as £99 a month. That’s fine, as long as your monthly budget has room for £99 in it.

Remember £99 isn’t all you’re going to pay. There’ll be more finance costs (see below) and other associated running costs such as insurance, tax, servicing and maintenance plus fuel.

Look at the total cost of car finance

Rather than basking in how little the headline figure is (that’s what whoever is providing the finance wants), look at what the total monthly cost is. That is including the deposit, a final payment (if applicable), the interest you’ll pay and any other arrangement charges or similar. You can then divide this by the number of months of the loan and find out a real monthly cost.

Thankfully, when car makers show finance projections on their website, they have to show the total cost plus all the add-ons too.

Look at the example

At the time of writing, Toyota has a projection for an Aygo x-trend. If you want £99 monthly repayments, you have to pay a £3910 deposit (Toyota gives you a further £500 ‘allowance’). There’s a 0% APR so just to run the car for 48 months, it’ll cost £180.45 month. If you want to buy the car outright, you must put up a £4027.50 final payment. The result adds up to £272.71/month over four years.

How much is the deposit/mileage limit?

There are two way to lower your monthly payments: increase the deposit or lower the number of miles you expect to cover. But not everyone has a few grand hanging around to pay a large deposit or the flexibility to reduce the number of miles they cover.

Are there any penalties?

All elements of finance are worked out on what the car will be worth at the end of the deal. This is because whoever is providing the finance will own the car at the end of the term. Unless of course you buy it on a Personal Contract Purchase and decide to buy the car outright. But even if you do, what you pay will have been worked out according to the car’s value at the end of the deal.

The number of miles the car has covered has a direct relation to its value. When you take out finance you agree on a set number of miles per year or over the lifetime of the deal. You then pay a penalty for exceeding these. Penalties are usually between 4p and 10p per mile. That might not sound much but if you exceed the agreed mileage by a few thousand every year, the penalty could end up being hundreds of pounds. If you think you’ve been charged too much for a PCP or PCH, you can contact the Financial Conduct Authority.

Think about equity in the car

Ideally you want to have what’s known as equity in your car when you come to the end of a finance deal. This is when you give the car back and you’ve paid more in repayments than the car is currently worth. You can then put this equity towards the deposit on another car. But the lower the headline monthly payment, the less likely it is that you’ll build equity in the car. And some dealers have been known to set monthly payment rates artificially low to secure a sale, knowing that come the end of the loan, the driver won’t have any equity to put towards a replacement.

Which is the best way to own a car?

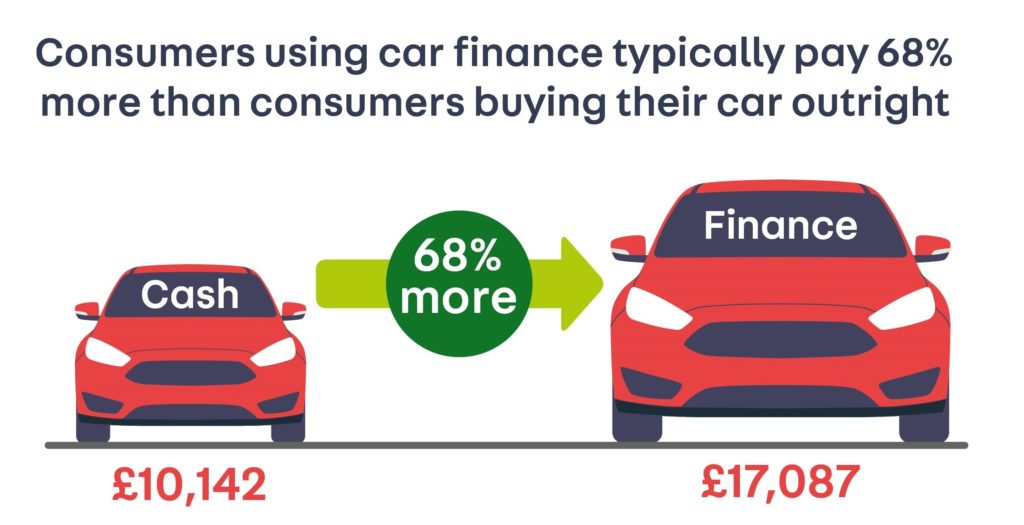

As always, buying a car with cash is the cheapest overall way. But then it does tie up a large sum.

PCP is the more popular because of the flexibility it offers. But PCH is catching up because it’s cheaper. If you’re in a stable financial position to be able to afford the payments and you’re not expecting your circumstances to change, PCH could be the way forwards. Any doubts about those and you need a PCP.

But buy any motor on car finance and it can tie you in for three to four years, during which time life can change. You might lose your job and not be able to keep up the repayments. Or your family requirements could alter and you might need a different sort of car.

I’ve been writing about cars and motoring for more than 25 years. My career started on a long-departed classic car weekly magazine called AutoClassic. I’ve since pitched up at Autosport, Auto Express, the News of the World, Sunday Times and most recently the Daily Telegraph. When I’m not writing about cars and motoring, I’m probably doing some kind of sport or working in my garden.